Key Takeaways:

- Dermatologists invest a lot of time into their education and earn multiple six figures.

- Disability insurance for dermatologists can protect you and recover a portion of your income.

- Getting a true-own occupation policy and the right coverage is key.

Deciding to study dermatology and focus on the body’s largest organ — skin — can mean investing over a decade into making your dream career a reality. Dermatologists who pursue this path undergo extensive education and training, taking about 12 years to become a dermatologist.

As part of that investment, you’re rewarded with a pretty comfortable salary. According to data from the Bureau of Labor Statistics (BLS), the average wage for dermatologists was $302,740 per year as of May 2021.

This can be a great way to make a living, but if an injury or illness arises that affects your hands, eyes or body, it could make your job difficult or impossible. Although this is difficult to think about, you can take proactive steps and protect yourself from a loss of income with the right financial tools.

In this guide, we’ll cover what you need to know about disability insurance for dermatologists. Through SLP Insurance and our partners, you can get own-occupation coverage. If we can’t help, we’ll refer you to the right place, even if we won’t earn money from securing your business. Read on for more information and to get a quote.

Why do dermatologists buy disability insurance?

Disability insurance is a type of insurance coverage that can help provide some of your income as a benefit, for a set period of time, in the event of illness, injury or disease. Your benefit generally depends on the type of policy you get and the coverage period. In some cases, you might receive disability insurance benefits until retirement age.

Although disability insurance is a smart idea for nearly everyone, it’s especially important for dermatologists who rely on their eyes, hands and physical faculties to perform exams and procedures. Losing out on the ability to earn that level of income due to illness, injury or disease can add extra stress and heartache to an already challenging situation.

Being prepared is key. The statistics around disability might surprise you. Based on information from the Centers for Disease Control and Prevention (CDC), 1 in 4 adults in the United States has a disability. Also, the Council for Disability Awareness notes that 1 in 4 people who are 20 years of age will become disabled by the time they retire. The same report also states that long-term disability is typically related to more common ailments like cancer, heart disease, and back injuries.

What should dermatologists disability insurance cover?

Dermatologists can look into short-term disability coverage and long-term disability coverage. Long-term disability coverage provides the most protection, and you can choose a policy that offers a payout based on your preferred time frame.

Given that dermatologists help treat patients with skin conditions such as dermatitis or a rash and may perform procedures such as removing warts or skin cancer, it’s important to consider the following as part of your disability insurance.

Own-occupation

When getting disability insurance for dermatologists, it’s crucial to get own-occupation coverage. This means that if you’re unable to perform work in your own occupation, you’ll be eligible for benefits. Other types of coverage might determine that as long as you can work a different job, you won’t qualify for benefits.

Under own-occupation coverage, even if you’re capable of working a job that’s outside of your primary occupation, you can still qualify for disability benefits. This is important as dermatologists spend 12 years training to work in their specialized field, and this is a surefire way to help protect that investment.

Future increase

If you want even more protection when getting disability insurance, opting for a future increase rider is a smart idea. This offers policyholders the ability to secure additional coverage later on without a medical exam. If you face a health issue in the future, you can still purchase more coverage.

Student loan rider

Pursuing your higher education to become a dermatologist can mean taking on a huge amount of student loans. Student Loan Planner® found that dermatologists tend to owe multiple six-figures of student loan debt.

What happens if you have student loans and become disabled? If you have federal loans, you might be eligible for Total and Permanent Disability discharge.

A student loan rider may also help you. The student loan rider generally comes with a 10- or 15-year term from when you sign up for the policy. To make sure it makes sense, review minimum and maximum benefits for this particular rider. Your student loan payments are then processed and made to your lender.

Residual disability benefits

In many of these cases, you must demonstrate full disability to qualify for benefits. But if you opt for residual disability benefits and can still do some kind of work, you might still be able to receive benefits with a partial disability.

For residual disability benefits, you might receive the full total-disability amount for a set period. Once that period is over, the payment amount might be based on a percentage of your income.

Getting proper coverage and the appropriate riders, as needed, can set you up for success. In the event of disability, you might be eligible for Social Security disability benefits. This benefit likely isn’t enough, though.

Based on Social Security Administration (SSA) data, the average monthly benefit as of October 2022 was $1,364.41. The federal poverty level for one person as of 2022 stood at $13,590, which comes out to $1,132.5 per month. In other words, relying solely on Social Security for disability coverage could potentially get you a couple of hundred dollars more than the current poverty level.

Downgrading your lifestyle or experiencing high stress about money during an already stressful time isn’t ideal. That’s why getting your own disability insurance policy can ensure that you receive a higher percentage of your income so you can take care of yourself financially.

Consider your fixed housing costs such as a mortgage payment, student loan payment, car payment, and any other financial obligation that is necessary or important to you. As high-income earners, dermatologists can protect more of their income with the right disability insurance coverage.

It’s important to note how dermatologists are viewed by insurance providers. Although this profession isn’t as high-risk for an injury as other doctors, those who perform more invasive procedures tend to have more risk factors and pay a higher premium.

What kind of disability insurance coverage is offered to dermatologists?

Dermatologists might have various types of disability coverage available to them. Some examples include the following.

Disability insurance from your employer

Depending on your employment situation, you might be offered disability insurance through your workplace. If that’s the case, look at whether it’s short- or long-term coverage, and how much you’d actually receive in benefits. If you become disabled and get benefits through a group, it might be considered taxable income, according to the Internal Revenue Service (IRS).

Dermatologists with their own private practice DIY their own benefits, so they wouldn’t have access to something similar. That’s why it’s crucial to fill in the gap in coverage and get disability insurance to cover your bases.

Professional associations

Doctors like dermatologists can look into group disability insurance through professional associations such as the American Medical Association (AMA). This is through a specific group and catered to physicians to score the best rates.

More specifically, dermatologists can look for disability insurance through the American Academy of Dermatology Association which partners with Aon Affinity Insurance Service Inc. to provide coverage.

Individual policy

It’s possible to purchase an individual disability insurance policy through a broker. An insurance agent can assist you in finding a policy that works for your financial situation and level of risk. Many of these policies may come from what’s referred to as “The Big 6” which are the top companies providing own-occupation coverage. These include:

- Ameritas

- Guardian

- MassMutual

- Ohio National

- Principal

- The Standard

Guaranteed Standard Issue (GSI)

Guaranteed Standard Issue refers to a type of coverage you may not hear about that often. That’s because it’s typically not discussed by brokers and is generally only available for a certain population — those in residency or a fellowship program. Unfortunately, attending dermatologists typically don’t qualify for this option.

Through this option, policyholders get guaranteed coverage without asking any medical questions. Dermatologists in residency or fellowship who have a pre-existing condition can find coverage this way. In other cases, it can be a great way to get discounts and affordable coverage.

There are many places that provide GSI policies, including:

- Johns Hopkins

- UC Davis

- Louisiana State

You might be eligible for some discounts as well, which can vary. Women tend to pay more for disability insurance and some providers offer unisex pricing, which can be advantageous.

SLP insurance is committed to helping you get the best policy for your situation, whether it’s with our partners or not. To get a customized quote for disability insurance, complete the form below, and a partner agent will reach out with next steps shortly.

Get Your Own-Occupation Disability & Term Life Quote

What insurance coverage do you want a quote for? (check all that

apply)

Step 1: Job

Step 2: Health

Step 3: Your Info

What is Your Occupation Status Currently?

NEXT

Height

Weight(lbs)

Have you had any recent surgery or hospitalizations?

Do you take any medication?

Do you have any medical conditions?

NEXT

How much disability insurance do dermatologists need?

Dermatologists earn an average of $302,740 per year, according to BLS data. Disability insurance doesn’t replace all of your income, but a percentage, generally between 50% to 70%. Let’s say on average disability coverage replaces 60% of average income.

If you earn the average dermatologist’s salary, you’re earning about $25,228 per month. If you get disability coverage that covers 60% of that income, you may qualify for $15,137 per month.

That can help a lot. For dermatologists who have a medical specialty, that income could be even higher and may need higher amounts of coverage. Below are some dermatology specializations alongside the maximum benefit available given the salary.

Dermatopathology, $525,000 | |

Pediatric dermatology, $351,000 | |

Cosmetic dermatology, $326,508 |

In other words, you might need more disability insurance coverage than you think to maintain your lifestyle, and avoid financial stress. Below we cover how to find the right amount for your situation.

Dermatologist disability payout amount

When getting disability insurance for dermatologists, it’s key to get the right payout amount. Given the examples above, the payout may be around 60% of your income. So for the average dermatologist, you can expect to qualify for up to around $15,000+ per month in benefits. When you purchase disability coverage on your own and pay with after-tax dollars, these benefits are paid out tax-free.

Ideally, benefits should cover housing costs, daycare, loan payments, and more as a buffer. If you’re the breadwinner or sole earner, you might want to apply for higher amounts of disability coverage.

Dermatologists disability insurance premium cost

How much you pay for disability coverage depends on a number of factors including your current age, health history, state, occupation, and whether you’re a smoker or non-smoker. As a dermatologist, if you practice more invasive procedures, compared to non-invasive procedures, your premiums are likely higher. Generally, you can expect to pay between 2% to 4% of your income for a long-term disability insurance plan.

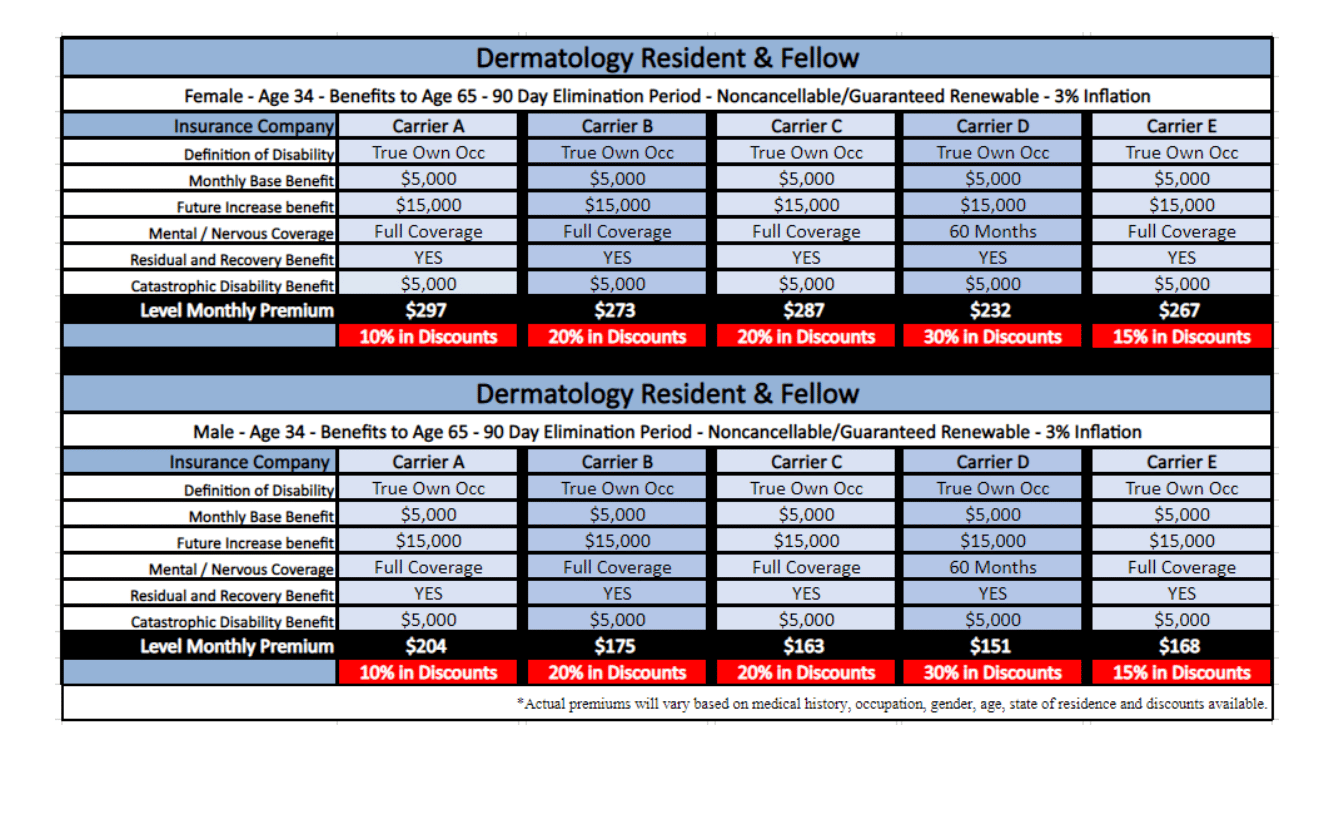

Source: SLP Insurance LLC

The chart above includes prospective rates from partner PKA Insurance for dermatology residents and fellows. As you can see, for a base benefit of $5,000, premiums could range from $151 to $297 depending on gender and carrier.

Discounts are typically available for residents and fellows. Discounts might be possible if you’re an attending physician, but will need to go through underwriting and medical review to qualify. Also, please note that some carriers put a time cap on benefits if the disability is related to mental or nervous disorders.

Why you need to review your dermatologist disability insurance policy

Getting disability insurance for dermatologists is a smart way to protect your income. But there are factors to consider and review ahead of time.

- Review true own-occupation policy language to make sure it’s a good fit. Work with an expert and make sure their definition of own-occupation works for you.

- Understand what is considered a disability — ask about its definition of disability as it relates to various scenarios.

- Assess the maximum monthly benefit so you understand your potential disability income.

- If you have a pre-existing condition, work with someone that will always cater to your interests and needs.

- Always compare policy prices as you might be paying too much.

- Make sure you have the appropriate coverage. If you have group disability coverage with an employer, it might be woefully insufficient. Don’t risk not being able to stay in your home or pay your bills.

Get a disability insurance quote for dermatologists

You’ve worked hard and invested so much time into a dermatology career that helps others. To help protect yourself and your finances, you can apply for disability insurance for dermatologists through SLP Insurance.

SLP Insurance and its partner agents provide true-own occupation disability coverage and can refer you to a different broker if we can’t help. We make sure you get any discounts you might qualify for, and provide customized quotes for your situation. Fill out the form below to get a quote and our team will be in touch!

Get Your Own-Occupation Disability & Term Life Quote

Step 1: Job

Step 2: Health

Step 3: Your Info

What is Your Occupation Status Currently?

NEXT

Height

Weight(lbs)

Have you had any recent surgery or hospitalizations?

Do you take any medication?

Do you have any medical conditions?

NEXT

{kind=link}